It has been an eventful seven weeks since the start of the banking crisis. We recently lost another previously well-regarded, well-managed, risk-averse bank. We will likely lose more, potentially many more. [0] And so many now have a simple question: Why?

After some bloviating by institutional actors early in the crisis, consensus is slowly pivoting from an indictment of individual banks’ management teams to recognition of a structural issue: when interest rates rise, asset prices fall. Banks loaded up on (good!) assets in a low-interest rate environment while flush with deposits, interest rates rose, banks became notionally insolvent or close to it, and deposits fled in a series of classic bank runs.

The only thing new under the sun is the size and speed of the deposit flight. A few weeks ago this was blamed on concentrated depositor bases all talking to each other on WhatsApp and maybe some shadowy cabal-like behavior by VCs. This explanation grows more farcical with each additional failure, so without admitting that they were previously talking out of their hindquarters, pundits and regulators are now focusing on… mobile apps.

I am darkly amused, as a sometimes financial technologist, that putatively serious people think that low-latency telecommunications technology is an exciting and unprecedented development for finance. My brother in prudential regulation, do you know why we call it a wire transfer?!

Anyhow.

Many, including those in corridors of power, are extremely perplexed that interest rate risk could surprise bank management teams, of all people. The essence of banking is, of course, maturity transformation; “borrowing short and lending long.” This necessarily exposes banks individually and the banking sector as a unit to interest rate risk. Moreover, banks are levered to that interest rate risk, because of course they are. How could banks have not known, etc etc.

Matt Levine has an excellent explanation of two financial theories of banking, one in which this risk is front-and-center and one in which it is swept under the rug.

I have not seen a sympathetic explanation of how well-intentioned, smart people could actually intentionally take the risks that resulted in the present crisis. Past advocates for that risk-taking might be understandably reticent about advancing their arguments for raising on the flop now that we’ve seen the river. So I thought I’d provide a sketch of the world as we understood it until very recently.

Brief disclaimer: I am an advisor at Stripe, and previously worked there for many years. Stripe doesn’t necessarily share my opinions.

I was also a depositor, creditor, and shareholder of First Republic Bank until their receivership. They never gave me anything other than their standard publicly available offers, but their standard offer was quite generous. (I might write about them specifically some other time, because there is a mix of a heartwarming story, some measured risk-taking in the loan book, a well-planned and well-executed deposit growth strategy, and then collapse mostly but not entirely unrelated to those other things.)

Natural hedges

Most readers will be familiar with the concept of financial hedges: an instrument designed to cover an exposure that one has but doesn’t want. There exist many different instruments that can be used for this purpose. See the rest of the Internet or your financial advisor of choice for much more on this topic.

After you have the concept of a financial hedge in your mental toolbox, extend that to the concept of a “natural hedge.” Instead of opening up Excel and doing complicated financial engineering, you have an exposure which is structurally equivalent to a financial hedge but caused by how your life or business interacts with the world.

Perhaps an example will help clarify: many businesses in Japan have an unwanted exposure to currency risk, specifically on the yen/U.S. dollar pair. The value they produce in the world is mostly denominated in yen, and their obligations to stakeholders are mostly denominated in yen, but important costs for their businesses, like commodities sourced overseas, are denominated in dollars. In futures where the dollar appreciates against the yen, they suffer windfall disutility. They didn’t set out to be currency speculators but suffered anyway, because that is the hand the world dealt them.

I run a business in Japan which, like many exporters, has a quirky characteristic: the future value I produce in the world is denominated in my choice of yen or dollars. I still need yen to pay my mortgage and keep the lights on, but in a world where the dollar appreciates against the yen, I experience windfall positive utility. I did not set out to be a currency speculator, but I would benefit anyway. (The “What happens if the yen appreciates against the dollar?” discussion would be long and nuanced from a business management perspective but accept for the purpose of this illustrative example that I’d be ambivalent about it happening. Car companies are the usual example used here, but there is a massive asterisk for them, too, and we are already several tangents too deep to follow up on it. [1])

This is a natural hedge.

Now imagine that my business were, oh, an order or two of magnitude larger than it actually is. I’d have a slightly better-paid and much better-dressed bank salesman than I factually do. And he might suggest: “Mr. McKenzie, you currently own something which has great value to the world but relatively little value to you: the windfall utility you’d reap in futures where the dollar appreciates against the yen. It is this beautiful asset, it decays over time, and you are doing nothing with it. Nothing! This offends my sensibilities as a bank salesman.”

“Now I happen to represent a team of geeks with the very finest MS Excel skills, and a team of other salesmen who spend every day talking to Japanese entrepreneurs with exactly the opposite exposure to your natural hedge! So can I buy it from you, for a bit less than my geeks tell me it is worth? The future will be here before we know it, and by then the option value implicit in that hypothetical windfall will go to zero. I will pay you cash money right now, or spread over the next few years, or whatever creative alternative we can agree on, to buy you out of that hedge. Then my colleagues will sell it to businesses who would experience currency pain more acutely than you do. We collect a spread for my ingenuity in pitching you, for having a huge balance sheet that will insulate you and those entrepreneurs from each other, and for employing the right combination of geeks and well-dressed salesmen in Tokyo. I, of course, collect a commission or bonus from my employers. This is a win-win-win-win.”

Now you might have some prior expectations that most entrepreneurs given this pitch by a bank salesman should run screaming. Maybe I agree and maybe I don’t, but regardless, variants of this pitch will be made today in Tokyo and New York and London and just about everywhere else complicated realities of businesses meet uncertainty about future world states.

Now, what if I were not the person holding the natural hedge? What if the holder was, I don’t know, a regional bank in the U.S.? Would a bank salesman try to make the sale?

Of course they would.

Deposit franchises as an asset

“Deposit franchise” is a term of art in banking that, much like “goodwill”, attempts to make legible and tangible out of a valuable idea which would otherwise just be a free-floating vibe. It means, loosely:

Some people in our local community have money and want banking services. We want the right to use their money and will bank the heck out of them to get it.

We rolled up our sleeves. We negotiated high-quality curb cuts with responsible transportation engineers. We leased up branch locations at the best intersections. We hired salesmen and taught them to wear suits. We gave away free coffee. We invited the general public to come in. We opened checking accounts for almost anyone who asked. We hired floors upon floors of professionals to deal with unglamorous expensive bullshit like mediating a Regulation E dispute between a tenant and landlord over an electronically presented check, a service we charge neither for and cannot stop providing or we all go to prison. We sponsored the Little League team. We send somebody out to the middle school twice a year to give a lecture.

And why? Because our loans business needs a low-cost stable funding source. And so we went out and built it, by the sweat of our brow. We built it with bricks and contracts and ATMs and math and smiles. And, by God, it is now a real thing. It is now part of the social and economic fabric of this town. It is as real as the town itself is real.

You tell me that deposits are flighty? That I have contractually committed to giving all of these customers their money on demand? That they could go to zero on any given Tuesday? Yes, the town itself could go to zero on any given Tuesday. Every single person could, of their own free will, simultaneously decide to move, and we wouldn’t even have someone left to turn out the lights. But in the world we actually live in, that will never happen. The town endures. The deposit franchise endures. The bank endures.

This sketch is self-serving, but only in the sense that teachers think that defined benefits pensions are their just reward for educating the future of our nation is self-serving. Every business and every profession has its own internal narratives, which they genuinely believe and will happily tell you about.

Bankers believe that deposit franchises have value, real cognizable honest-to-financial-reporting value. They will happily tell you about this belief, at substantial length, including in their quarterly and annual reports. They will use words like “bedrock” to describe their “core deposits”, the ones which they attracted with their sweat and smiles (and, it must be said, cross-sold unpriced valuable banking services) rather than with making attractive economic offers to ruthless interest rate maximizers.

Now: how does one value this asset?

Convention in finance is that the value of assets is the sum of their future cash flows discounted for time to realization and uncertainty. We will elide the full net present value calculation for simplicity. But, following this sketch: the future cash flows from a deposit franchise are, mostly, net interest income earned from one’s loan book (and other balance sheet items like, say, high quality agency-issued mortgage back securities) funded at the margin from the low-cost deposits one expects to be able to raise in the future in the Monday through Friday sweat and smiles business.

The value of a deposit franchise increases with interest rates

This value goes up when interest rates go up, because net interest margin typically increases when interest rates rise. Why? One reason is that one’s operational costs are far less sensitive to interest rates than one’s pricing strategy; your computers and lawyers don’t become more expensive just one year Treasuries are 5% more expensive.

Another is that your deposit pricing has what bankers call “deposit beta.” In layman’s terms, this means that your sweat and smiles are sufficiently productive that you don’t have to pass through every marginal dollar of interest income to your depositors.

A brief aside about deposit beta

Many people have a model of banks where paying depositors is just something that banks must do. Until recently, I thought that hotels understood that hotels must have clean rooms every day by default. It turns out culture changed when I wasn’t looking.

“Phones got better over time and now people pay a lot more for them but are happier” is a simple story, agrees with voluminous data, and is uncontroversial. Substitute “banking services” and people become very upset about these claims. And they are “claims” in the sense that “cigarettes cause cancer” is a claim.

One of the interesting structural shifts in banking in the last twenty years has been an extended period for bank marketers, newly empowered with IT systems that don’t suck suck less than previously at many margins, to run tests on response curves in deposit pricing. Basically, how many more customers and how much more share of wallet do we get—how many more tens of millions of dollars can we borrow—at X bps of interest? How about X + 5? X + 25? X + 50? X + 100?

The results of these experiments surprised even many bankers: huge swathes of the population are entirely price insensitive, with regards to deposit pricing. So deposits have been aggressively repriced, relative to the short term funds rate.

Banks renegotiated the traditional covenant with regards to interest: they now keep almost all of it for almost all of the products they offer, as opposed to most of it for most of the products they offer. This was not negotiated in some smoky backroom by a conspiring cabal. It was decided in the clear light of day, accompanied by incessant disclosure to customers, and extremely explicitly publicly communicated to shareholders and regulators.

And so they were aggressively rolled out to many—not all, but many, including many of the most important—banking products, at firms of all sizes up and down the country. You can still aggressively use promotional pricing or high-cost funding sources, at some banks, in some part of their funding mix, but the world has changed.

Bankers would, in recounting this same set of facts, say something like:

“Our customers value their relationships with us. They have access to a crowded market with literally thousands of options for core banking services. Some of them aggressively compete with us on price. The best proof of the strength of our deposit franchise is that we win our customers’ business again every single day. Do we apologize for this? No, we do not.

Want proof that that the iPhone is a great product? Ignore the specs. Ignore the reviews. Ignore what your friends say. All that is noise. The proof is that you already know you’ll buy the next one before you hear the price.

Oh, incidentally, Apple decided to directly compete with us, including aggressively on price. We love to see it, much like we love to see school bake sales in town. And they gathered a whole billion dollars in deposits! Wow! Youth today are such go-getters.”

OK, enough of invoking that strawman. He’s ludicrously overconfident. You can listen to many of the reasons he’s wrong if you go out to dinner with fintech-focused venture capitalists, and you should pay close attention both to their persuasive arguments and also how they actually pay for dinner. [2]

Some economists at the Fed look at this same set of facts about deposit beta and describe it very differently than I would, for what it is worth.

The deposit franchise as a hedge

Suppose you’re a salesman and you’ve identified that the deposit franchise is a natural hedge. Bracket the question of whether you can convince the decisionmakers for the deposit franchise to do business with you. Who in the economy most needs an interest rate hedge? Who could you sell that to?

I claim that it is the mortgage industrial complex, and if you want me to be more specific, it is the government-sponsored entities (Fannie Mae, Freddie Mac, etc). They the housing market operating in the U.S. by providing securitization infrastructure which, as a side effect, backstops credit risk in conforming mortgages with the full faith and credit of the U.S. government. Agency mortgage backed securities (MBS) are the second largest dollar-denominated fixed income category in the world. They are much larger than minor players like “all corporate bonds combined.”

The only larger rates market is for U.S. Treasuries, but the production function for the United States federal government functions in effectively all interest rate regimes. This is very not true of mortgage origination. So this massively socially important apparatus needs to lay off interest rate risk every year, rain or shine. How much? Let me handwave and say “a few trillion dollars.”

It does so, in material part, by securitizing the mortgages and selling them to counterparties. Those counterparties now own the interest rate risk, leaving the mortgage origination industrial complex to continue facilitating home construction, sales of existing homes, job transfers, moves closer to relatives, etc.

So if you hypothetically had a set of actors who had a natural hedge against rising interest rates, could you find a contra desperate to buy that hedge from them at all possible sizes? Oh yeah. It’s extremely sophisticated and has worked for literally decades to lay all the institutional and infrastructural groundwork to facilitate this trade, too!

…

Now, if you cast your memory back to the high-quality assets of certain recently failed banks which suffered large mark-to-market impairments, do you remember their constitution? They were largely a mix of Treasuries and, hmm, wait a minute, a much larger amount of agency MBS.

SVB, ~$80 billion in MBS. Signature Bank, ~$20 billion. First Republic, only about ~$10 billion.

These portfolios increased in size materially during a period of low interest rates, backing up the truck on interest rate risk effectively, and then had a foreseeable outcome (billions of dollars in losses) when interest rates rose.

Again, we were subjected to much commentary about these banks being impressively poorly managed. I invite interested readers to pick a regional bank at random and look at their public reporting for how much agency MBS they hold. If that sounds like work, it’s not difficult to find curated lists.

As Ian Fleming once had a character say: “Once is chance. Twice is coincidence. Third time is enemy action.”

The enemy was ourselves.

Regional banks were instructed to load up on agency MBS

A claim which I feel might be dismissed as a conspiracy theory, and which I want to advance carefully:

It was the repeated advice of people in corridors in power, including bank boards, bank risk departments, and crucially bank regulators, that regional banks should buy more agency MBS at prevailing margins.

I express certainty that this advice was given verbally. You’ll forgive me for not saying how I know. I expect that this advice was entirely uncontroversial and given as a matter of course. Generals are great at fighting the last war and regulators are totally on the ball at preventing the last financial crisis.

We nationalized credit risk for mortgages, dawg, at substantial expense and requiring years of effort. You folks need to do your part and buy MBS to keep the economy moving, particularly during these troubled times. Sure you could e.g. make commercial loans but I’d be much more comfortable from a risk perspective seeing MBS at the margin than I would aggressive growth in the loan book. You need to deploy a surge in deposits? Just buy MBS.

This advice did not minimize for interest rate risk, to put it mildly. Society has many demands of the banking system and “Don’t take interest rate risk” is not very high on that list. (A computer can be perfectly secure if it is turned off and a bank can be perfectly neutral on interest rate risks if it simply doesn’t participate in credit creation. Plausibly you need a paperweight in your life and if so you can use either of those things.)

I express substantial confidence that there are voluminous written recommendations where this advice was made formally and explicitly. I expect a careful reading of reports from bank supervisors in the inevitable postmortems to this crisis will acknowledge that they’ve found these emails. This will be between much more prominent statements that will thoroughly throw bank management teams under the bus and proudly tout every time a subscore on a review was Conditionally Meets Expectations #nailedit. (I point interested readers to this document for the flavor of postmortems to come, while expressing an anthropologist’s careful neutrality with regards to the contents.)

I express certainty that there were formal incentive systems which encoded this recommendation. For example, one of many ways by which we regulate banks is by capital requirements. Different assets require different amounts of capital to carry them on the books, in a process called “risk weighting.” Since banks will optimize for return on capital, adjusting risk weights is a way to substantially guide their behavior via shaping incentives without directly mandating one’s preferred outcome.

This topic gets very wonky, so, spoiler alert: a quick perusal of risk weights, which are objective facts about the world banks operate in that you can present in a table, will show an enormous thumb in favor of MBS. Where is the corresponding table of concern for interest rate risks? To make a very long story short, while bank regulators notionally care about interest rate risk they care about it a lot less. The shape of our last crisis was about credit quality and counterparty risk rather than interest rates.

Our generals wrote our specs for these weapon systems to thoroughly address the inadequacies in previous weapons systems in the environment of previous wars; a shame we’re fighting in a new environment but that is sort of the way of things.

It was not an accident that banks loaded up on MBS. We wanted them to. We told them to.

We didn’t expect this to blow up a large chunk of the U.S. banking sector. We didn’t expect the rate hikes to blow up a large chunk of the U.S. banking sector. We knew they would cause losses, to banks and all other holders of financial assets, but modeled them as survivable and more palatable for society than continuing inflation was. We appear to continue to believe that, at least to the extent we believe we can have our cake and eat it too.

And, to be clear, as of this writing, it has not yet blown up a large chunk of the U.S. banking sector. But we are clearly in one of the hypothetical future universes where the U.S. regional banking sector selling its natural hedge has worked out very, very poorly relative to prior expectations. There are other hypothetical universes! In ones where we had no pandemic and no massive fiscal response and no inflation worries, they simply got paid handsomely for use of their deposit franchises to support society's important goal of making housing available and affordable!

Why did the hedge bust?

Clearly we overweighted the value of deposit franchises and their stickiness. Why did we do so?

There are theories that have been advanced for the banks which have failed so far, and they are idiosyncratic claims about particular deposit bases. Each additional failure should increase our confidence that we’re not seeing isolated stories that rhyme but are instead seeing one story, one structural story, roll out over a structural footprint. It arrives in different parts of those footprints at different rates, but it is just one story.

What is that structural story? I don’t think it is fully captured yet. But, if I had to take a guess at the biggest contributing factor, I have one for retail and one for sophisticated customers.

For retail, for a period of years—years!—we took the sweat and smiles business, the work of literal decades, and we—for the best of reasons!—said We Do Not Want This Thing. That very valuable thing was, like other valuable things like churches and birthday parties and school, a threat to human life. And so we put it aside. We aggressively retrained customers to use digital channels over the branch experience. We put bankers at six thousand institutions in charge of teaching their loyal personal contacts that you can now do about 80% of your routine banking on their current mobile app or 95% on Chase’s. And then we were shocked, shocked how many people denied the most compelling reason to use their current bank and shown the most compelling reason to bank with Chase switched.

With regards to sophisticated customers, the answer is not primarily about mobile apps or how difficult it is to wire money out of an account. It is about businesses making rational decisions to protect their interests using the information they had. Sophisticated businesses are induced to bring their deposit businesses, which frequently include large amounts of uninsured deposits, in return for a complex and often bespoke bundle of goods they receive from their banks. The ability to offer that complex and bespoke bundle is part of the sweat and smiles of building a deposit franchise.

Now, at the risk of stating the obvious, you must be able to deliver that bundle and the customer must trust your ability to do so now and in the near future. Sophisticated businesses know the deal they have struck. They know the risks to their business if you fail to be able to deliver on the services you have promised. This is the definition of being sophisticated.

Up until very recently, sophisticated businesses had little visibility into near-term risks to their banks’ ability to execute on the bundle. Their most material update came daily as the services were delivered just like the day before; their most potentially surprising update came quarterly, as the media digested and regurgitated the bank’s financial position for the business community’s benefit. (Most sophisticated businesses do not underwrite their banks quarterly. Of course they don’t. Why would they do that, when they are astoundingly unlikely to outcompete literally the entirety of capitalism at this exercise?! No, they just consume the outputs of the market, here as elsewhere.)

Why did they suddenly trust their banks less about the near-term availability of the bundle? Contagion? Social media? I feel these are misdiagnoses. Their banks suffered from two things: their ability to deliver the bundle was actually impaired. They had “bad facts”, in lawyer parlance. Insolvency is not a good condition for a bank to be in.

And those bad facts got out quickly, not because of social media and not because of a cabal but simply because news directly relevant to you routes to you much faster in 2023 than in 2013. There is no one single cause for that! Media are better and more metrics-driven! Screentime among financial decisionmakers is up! Pervasive always-on internetworking in industries has reached beyond early adopters like tech and caught up with the mass middle like e.g. the community that is New York commercial real estate operators.

And, of course, the network functions like a neural network. It is dynamic. Every time it “learns” that a previous routing of information was successful, for some definition of successful (and being first out in a bank run is a success!), it reconfigures edges and nodes to get better at that in the future. People learn which Twitter accounts get the goods six hours before the WSJ does. Some of them end up on lists. The people on those lists see the lists and become friends with each other! They get better at their jobs, sometimes notional and sometimes no really they work at Bloomberg this is absolutely the professional specialization they get paid handsomely to do, with each successive failure.

Which is great from an observability perspective and less great from the perspective that increasing observability of this particular system turns stress into failure at the margin.

Further bad news: the problem is bigger than MBS

As I’ve written repeatedly: fixating on security portfolios ignores that the same interest rate risk applies to the loan portfolio for any fixed rate loans.

This is a kissing cousin to the private equity practice of charging LPs to minimize their exposure to equity volatility by simply… not changing marks as their assets suffer the same slings and arrows that public equities suffer and almost instantaneously react to.

In both cases, there may actually be some social utility in this practice. But we should be institutionally aware that we’re doing it, right?

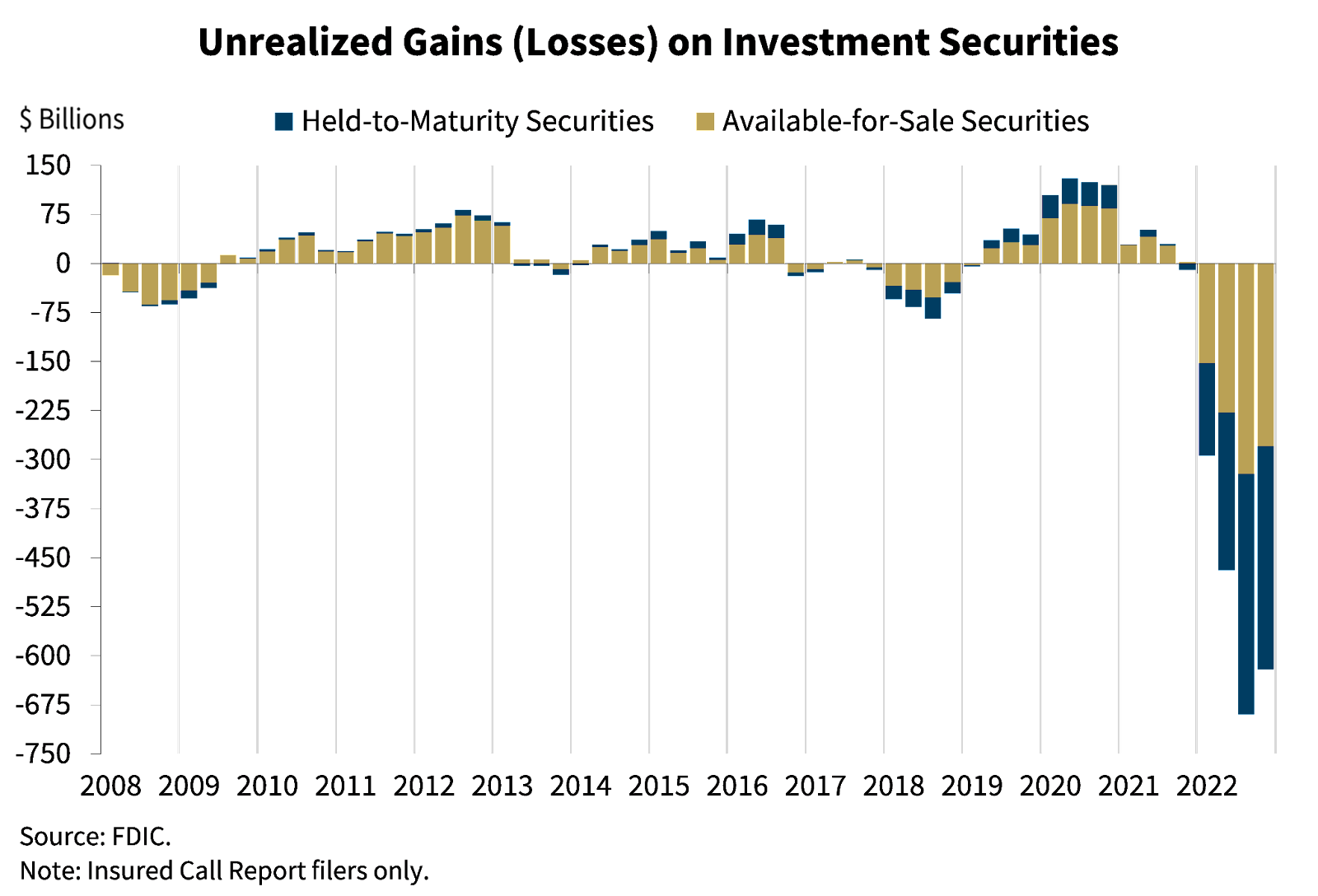

I think our level of awareness is less than where it should be at the moment. Partially this is for Seeing Like A State style reasons. Securities are so legible. They have conveniently surveillable mark-to-market prices and trade continuously. You can just look up the CUSIP on Bloomberg and see exactly how bad life has gotten. The FDIC can easily Excel aggregates into very concerning charts, like the gobsmacker from February:

Loans, on the other hand, remain quite illegible. First Republic wrote this geek a fixed rate loan in 2021. It doesn’t have a CUSIP and no web page anywhere lists how much it is impaired.

So I’ll take a guess. Some combination of First Republic shareholders and the FDIC insurance fund lost ~15 cents on the dollar of that loan, despite me continuing to pay as agreed, because Chase did not buy it at par. It is no longer worth par.

In the ordinary practice of banking, we ignore the notional loss on this loan. The loan will recover towards par over the remaining 5 years of its 7 year term.

If your bank is a going concern, you get to basically ignore many impacts of the random walk down interest rate futures. You make loans in all interest rate environments. Some of your vintages are worth more, some are worth less, but you’ll eventually collect almost all of the actual countable money. Your notional opportunity cost is strictly notional. Who cares? But if they’re not a going concern, bam, immediate 15 cent loss on my loan and every other loan from that multi-billion dollar vintage.

This combination of the focus on securities over loan books, the illegibility of loan books, and discontinuity in the realization of losses under conditions of stress makes me think that we have not yet come to grips with how bad the situation in the banking sector actually is.

And, pace our earlier discussion of learning, people who now understand the legible, convenient mechanics of how this scenario functions vis MBSs have now had a few months to do painful spreadsheeting and model out exposures of loan books across the U.S. banking sector.

It is no longer February

Many very intelligent people of good will are still living in February.

“Sure, there are some losses, but the losses are extremely survivable if the bank is adequately liquid and if depositors do not depart en masse.”

This was a very reasonable belief in February! If you had asked me, I would have eagerly agreed with it. I would also have laughed at the proposition that a well-regarded U.S. bank could see a hundred billion dollars of deposit outflows in less than a quarter or, say, $42 billion in a single day.

Now that both of those things have happened to different banks I have revised some views I was very confident of in February.

And now I am carefully reading updates with regards to deposit outflows and, well, expecting that some institutions which the public relies upon to accurately report deposit outflows might be other than perfectly candid with respect to what they know.

“Why didn’t the hedger hedge?!”

Many commentators have expressed surprise that banks loaded up on interest rate risk without hedging it.

I… am confused as to what instrument, and what counterparty, exists to hedge a one trillion dollar loss on a rates bet. You should have hedged, fine, assert that we roll back history to about 2019 and that society successfully identifies someone to take a one trillion dollar loss.

Is the proposal that we shouldn’t make trillion dollar interest rate bets? Cool, cool. You can have that belief, mortgages available in the U.S., and the Feds ability to do macroeconomic interventions, but you can only pick two of these three. Which are you willing to sacrifice? Note that you have to make this sacrificial pre-commitment upfront even in the face of the extraordinary conditions caused by a global pandemic and its economic sequelae.

So what do we do now?

I think the dominant probability is that we muddle through this. Tyler Cowen has a writeup of why one should expect this.

Concretely, “muddling through” means extraordinary public support for U.S. banks, such as via the Bank Term Funding Program, the de facto FDIC backstop for depositors of all sizes, and possibly additional mechanisms if things get worse. Will things necessarily get worse? I don’t want to be accused of spreading panic or talking down bank stocks, but if you model there being zero additional bank failures beginning today, you are welcome at my poker table any time.

Muddling through also means relatively low risk of widespread contagion from finance into the real economy. Real people will suffer; real people are already suffering. Banks are not blowing smoke when they talk about being woven into the fabric of their communities! But we’re less likely to see a 2008-style sharp, protracted worldwide disaster.

The banking sector will require recapitalization. One is welcome to their own estimate of it; DeMarzo et al (cited below) model between $190 and $400 billion of new private capital being needed. As I’ve said many times before, the sacred duty of bank equity is to take losses before depositors, and existing bank equity has absorbed very painful losses and will likely take more. [3]

Life will go on. It always does after financial crises.

Do you need to pay a lot of attention to this? As a retail user of the financial system, probably not that much, though you might want a backup bank account with one paycheck cycle worth of money in it.

If you are professionally responsible for financial infrastructure, you should know that sudden failures are more likely in times of stress and extraordinary action than they are in times not distinguished by stress or extraordinary action. That might counsel more attention to redundancy, risk management, and similar than you would pay if we were not experiencing a banking crisis.

[0] I point you to DeMarzo, Jiang, Krishnamurthy, Matvos, Piskorski, and Seru, whose paper Resolving the Banking Crisis includes the disquieting line “[T]he number of banks currently in the danger zone numbers in the thousands.” I do not know the degree to which one can usefully add to careful academic work by well-credentialed experts with “Oh yeah that agrees with my napkin math; glad someone important is saying it” but that does, FWIW, agree with my napkin math. I am glad someone important is saying it.

[1] OK, fine, since you asked: suppose you are a large Japanese automobile manufacturer. You do have partially benefit from a strengthening dollar because your cars will be cheaper in the U.S. market relative to your U.S. competitors. However, the cars you sell domestically are not fungible with the cars you sell in the U.S.

Moreover, and more importantly, you are severely constrained in taking full advantage of currency dislocations to reallocate production between Japan and the U.S., because you are a systemically important institution to the Japanese economy. If you forgot this fact—which you would not for a minute—Japan would begin an escalation pathway which starts with a friendly invitation to late-night whiskeys then winds through stern administrative guidance before going to much darker places.

Since that would be extremely unpleasant, you employ many talented people to do currency hedging. Some of them work for a bank which is, nominally at least, not a part of your corporate group. It is one of the largest financial institutions in the world and got there, in no small part, because you needed it to get there.

[2] ~90% chance of Chase Sapphire Reserve or Amex, according to my anecdotal observation in several hundred meetings with fintech professionals over about a decade and a half of orbiting the SFBA ecosystem.

[3] It’s always risky to read too much into price action, but as of this writing, “coordinated short attacks” are being blamed for volatility in the price of bank equity. I will reiterate that I do not short bank stocks, due to where I am in the information graph, but this point of view boggles my mind. There are some banks whose stock tickers price the equity of the business and there are others where it prices the option value of a very generous rescue package and/or miracle. I do not think one needs manipulation as a necessary ingredient in a positive expected value short thesis, to put it mildly.

Want more essays in your inbox?

I write about the intersection of tech and finance, approximately biweekly. It's free.